Key Findings

- The national average monthly cost for a home internet plan is $81.16. Prices range from $65.43 in New Jersey to $109.88 in Alaska.

- Though most households have not experienced recent internet service price hikes, nearly 1 in 4 Americans (23%) say internet bills stress their household budgets.

- 1 in 5 Americans (19%) worry about paying their internet bill each month; that number spikes to 41% among former ACP recipients.

- Women are nearly twice as likely as men to worry about affording internet service (24% vs. 14%).

- 1 in 5 households (19%) say their current internet plan doesn’t meet their needs, rising to 28% among former ACP households.

Home internet is so fundamental to daily life that it barely registers as a subscription anymore. Now, it’s an essential utility, on par with electricity and running water. Yet as household budgets remain stretched from years of elevated prices, a growing share of Americans are quietly straining under the weight of their monthly internet bill. However, this is one cost they cannot afford to cut.

This report is based on a BroadbandNow survey of 954 U.S. adults conducted in March 2026, combined with our analysis of active plans from more than 2,100 internet providers. It examines what Americans actually pay for home internet by state, how stressed they are about that cost, whether their service meets their needs, and what the ongoing fallout from the June 2024 end of the Affordable Connectivity Program looks like two years later.

What Is the Average Cost of Home Internet in the U.S.?

The average American pays $81.16 per month for home internet, or about $973 per year. But that national average masks enormous variation. BroadbandNow analyzed active internet-only residential plans across more than 2,100 providers to calculate average costs by state as of March 25, 2026. The results reveal a market shaped less by consumer choice and more by geography and the presence (or absence) of competition.

Average Monthly Home Internet Costs by State

| State | Average Monthly Price |

|---|---|

| Alaska | $109.88 |

| Iowa | $93.15 |

| Nevada | $89.12 |

| Georgia | $88.35 |

| North Dakota | $87.71 |

| Colorado | $86.70 |

| Montana | $86.37 |

| Missouri | $86.19 |

| Wisconsin | $84.82 |

| Kansas | $83.14 |

| Washington | $83.11 |

| Texas | $83.05 |

| California | $82.89 |

| Maryland | $81.91 |

| Oregon | $81.73 |

| Indiana | $81.29 |

| South Dakota | $81.14 |

| Minnesota | $81.04 |

| District of Columbia | $80.64 |

| Tennessee | $80.32 |

| North Carolina | $80.07 |

| Arkansas | $78.45 |

| Massachusetts | $78.37 |

| Idaho | $78.03 |

| Michigan | $77.85 |

| South Carolina | $77.85 |

| Pennsylvania | $77.74 |

| Kentucky | $77.72 |

| Illinois | $77.45 |

| Arizona | $76.82 |

| Virginia | $76.68 |

| New York | $76.47 |

| Alabama | $76.45 |

| Louisiana | $76.44 |

| Vermont | $76.17 |

| Florida | $76.11 |

| Ohio | $75.95 |

| Oklahoma | $75.93 |

| Utah | $75.54 |

| Mississippi | $75.35 |

| Nebraska | $75.34 |

| New Mexico | $73.56 |

| Delaware | $73.02 |

| West Virginia | $72.78 |

| Wyoming | $71.51 |

| Maine | $71.30 |

| Hawaii | $69.14 |

| Puerto Rico | $66.98 |

| Rhode Island | $66.55 |

| New Hampshire | $66.09 |

| Connecticut | $65.50 |

| New Jersey | $65.43 |

Source: BroadbandNow.com analysis of active internet-only residential plans from 2,100+ providers, as of March 25, 2026

Alaska is the most expensive state for home internet at $109.88/month, a 68 percent premium over New Jersey’s $65.43 average, which is the lowest in the nation. The highest-cost states tend to be those with fewer provider options, limited infrastructure, and significant rural populations. Meanwhile, densely competitive Northeastern markets, including Connecticut, New Hampshire, and Rhode Island, consistently appear at the bottom of the list, reflecting the downward pricing pressure that comes with robust ISP competition.

Why are some states so much more expensive for internet? Limited ISP competition is a well-documented driver of high broadband prices. Our own research on broadband competitiveness found that where fewer providers compete, prices stay high.

States like Alaska, Montana, and the Dakotas face structural disadvantages: sparse populations, difficult terrain, and high infrastructure costs that keep prices elevated regardless of consumer demand. While the FCC’s National Broadband Map has highlighted coverage gaps and low-competition zones across these frontier states, our research has consistently found that these gaps are even larger than the FCC initially reported.

Home Internet Is an Essential Utility, Not a Luxury

Before examining the financial strain from internet costs, it’s worth noting exactly how essential home connectivity has become. We asked survey respondents what they had done online in the past 30 days. The answers read less like a list of leisure activities and more like a checklist of modern life.

Online activities completed in the past 30 days

| Which of the following activities have you done online in the past 30 days? | Percent of respondents |

|---|---|

| Online banking | 89% |

| Shopping | 89% |

| Streaming video/TV | 87% |

| Playing online games | 60% |

| Work tasks for a job or business | 57% |

| Health care tasks (telehealth, patient portal, refills, test results) | 49% |

| Video calls | 46% |

| Job search | 31% |

| Government services | 20% |

| School or homework | 13% |

| None of the above | 0% |

Source: BroadbandNow survey of 954 U.S. adults. Multiple responses allowed.

Nearly nine in 10 Americans banked, shopped, or streamed in the past month. Half used the internet for healthcare, including telehealth visits, prescription refills, and test results, and nearly one in three used it to look for a job. These are not discretionary behaviors. They are the building blocks of financial stability, health management, and civic participation.

The study revealed that women were even more likely than men to use the internet for healthcare tasks (55 percent vs. 42 percent), a difference with real implications for the cost of service disruption or degradation for this population.

Primary method of getting online at home

| What do you primarily use to access the internet? | Percentage of respondents |

|---|---|

| A home internet plan (cable, fiber, DSL, fixed wireless, or satellite) | 88% |

| A cell phone plan, mobile hotspot, or 5G home internet device | 9% |

| Someone else’s Wi-Fi (family or neighbor) | 2% |

| Free public Wi-Fi (apartment, library, coffee shop) | 1% |

| I do not have a regular way to get online | 0% |

Source: BroadbandNow survey of 954 U.S. adults, March 2026

88 percent of respondents in our study rely on a traditional home internet plan as their primary connection. That means the cost and quality of that single service directly determine whether they can bank, attend telehealth appointments, or complete coursework. The nine percent who rely on mobile data face higher per-gigabyte costs and a greater risk of throttling.

The argument that “people can just use their phones” as a substitute for home broadband is not supported by the data. A telehealth appointment, a full remote workday, or a student completing online coursework simply cannot run reliably on a throttled mobile hotspot.

Americans Worry About Internet Bills Though Prices Haven’t Spiked

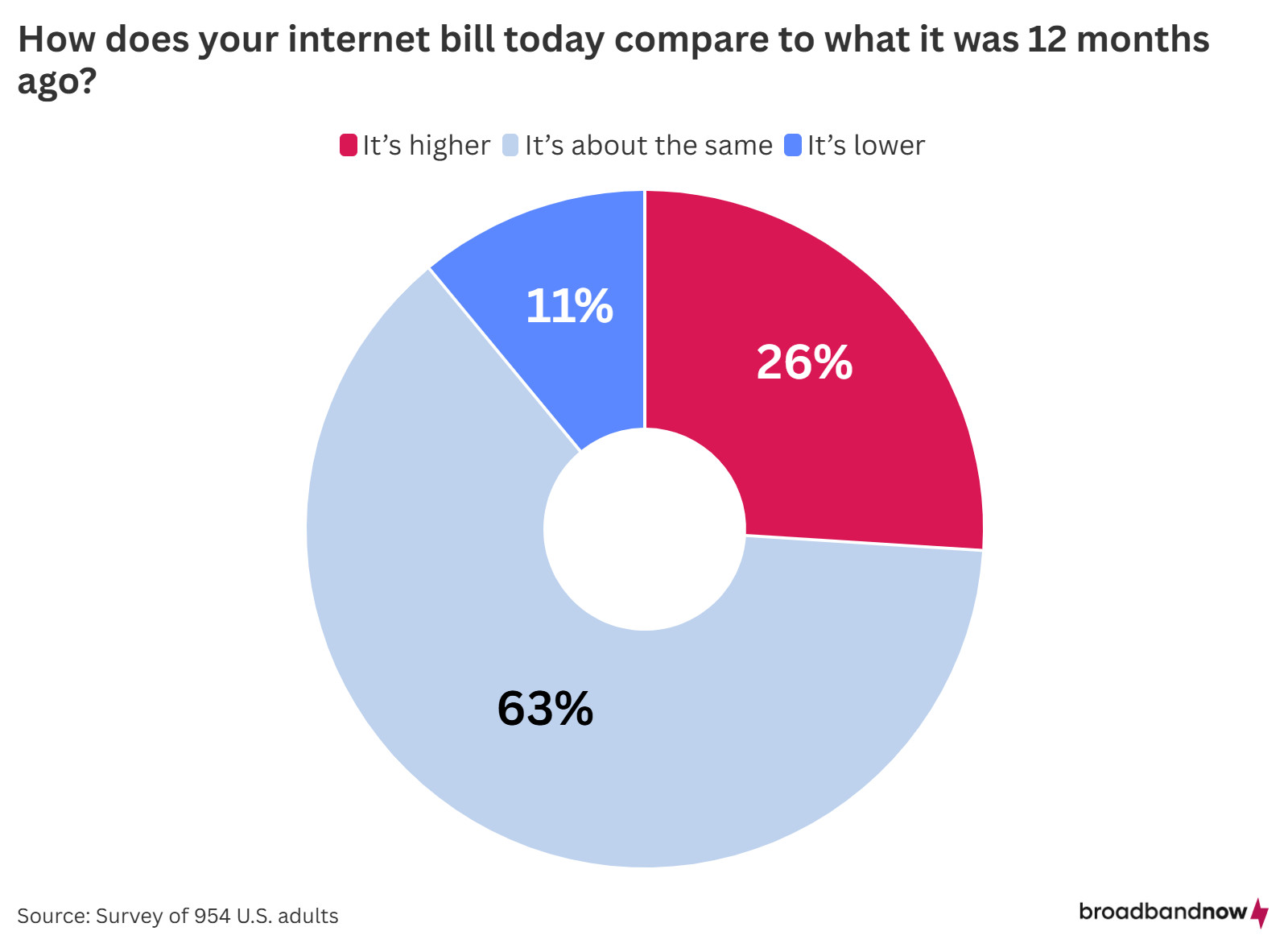

Unlike groceries, rent, and healthcare, broadband prices have remained relatively stable in recent years, and in many cases Americans are getting faster speeds for the same or similar price. New research from the Phoenix Center, a non-partisan research organization, found that broadband prices have actually fallen as speeds have climbed. That’s a meaningful distinction in an era of persistent inflation. Yet 1 in 4 Americans still report paying more for home internet than a year ago, and a growing share worry about covering the bill.

Though internet costs have not surged, the rising costs of many other goods have squeezed household budgets to the point where even a stable internet bill feels harder to absorb. When you’re spending more on food, housing, and energy, a monthly internet expense that once felt routine can start to feel like a burden, especially when it’s a bill you can’t cut.

Despite that context, Americans aren’t easily switching providers or cutting service when costs feel unmanageable.

More than one in four Americans report paying more for home internet than a year ago, yet two-thirds (67 percent) took no action to try to lower the cost. This isn’t necessarily consumer complacency. It could reflect a lack of meaningful alternatives in many markets. In fact, we found that 96 percent of U.S. counties have highly concentrated internet markets, meaning there is very little competition. In areas where only one or two providers serve, switching isn’t really an option.

Household actions taken related to internet service in the past 12 months

| In the past 12 months, which of the following actions has your household taken related to your internet service? | Percent of respondents |

|---|---|

| Switched home internet providers | 12% |

| Upgraded our home internet plan’s speed | 11% |

| Changed to a cheaper home internet plan | 10% |

| Bundled internet with another service | 8% |

| Downgraded our home internet plan’s speed | 3% |

| Canceled home internet service | 2% |

| None of the above | 67% |

Source: BroadbandNow survey of 954 U.S. adults. Multiple responses allowed.

Younger Americans (18–29) are the most active in managing their internet costs: they switch providers at nearly twice the rate of older age groups (17 percent vs. 10 percent). According to our study, they were more likely to upgrade their internet plans in the past 12 months, possibly reflecting greater comfort navigating provider options alongside stronger demand for high-performance plans. Younger Americans may also be more likely to move residences for educational or job reasons, which would make them more likely to switch ISPs.

Only five percent of all households downgraded or canceled service entirely, reinforcing that, for most Americans, home internet is a non-negotiable expense rather than a discretionary one.

Women and Lower-Income Americans Worry Most About Internet Affordability

Affordability anxiety around home internet is not uniformly distributed. Our survey reveals a clear pattern: women, middle-aged adults, and lower-income households bear a disproportionate share of financial stress in paying their internet bills.

Women (24 percent) were significantly more likely than men (14 percent) to report concern about affording internet service, a gap that likely reflects broader income disparities between the genders. Women are more likely to be solo parents and multi-generational caregivers, making reliable internet access for telehealth and schoolwork particularly critical. Nearly one in three (32 percent) lower-income households expressed concerns about internet costs, compared to 20 percent among middle-income households ($50K–$74,999). Age played a role, too: adults 45–59 were more likely to express worry than those 18–29, who may benefit from family subsidies, college dorm residence, or shared costs with roommates.

Nearly one in four Americans (23 percent) say internet costs actively stress their household budgets, and nearly one in five (19 percent) say their internet service doesn’t meet their needs. When that many people feel financial pressure around what is effectively a utility, it becomes a public health and equity issue, not merely a consumer preference issue. Brookings Institution research has found that because broadband access affects nearly every social determinant of health, barriers to affordability and adoption represent significant challenges to individual and community-level outcomes, from healthcare access to educational attainment.

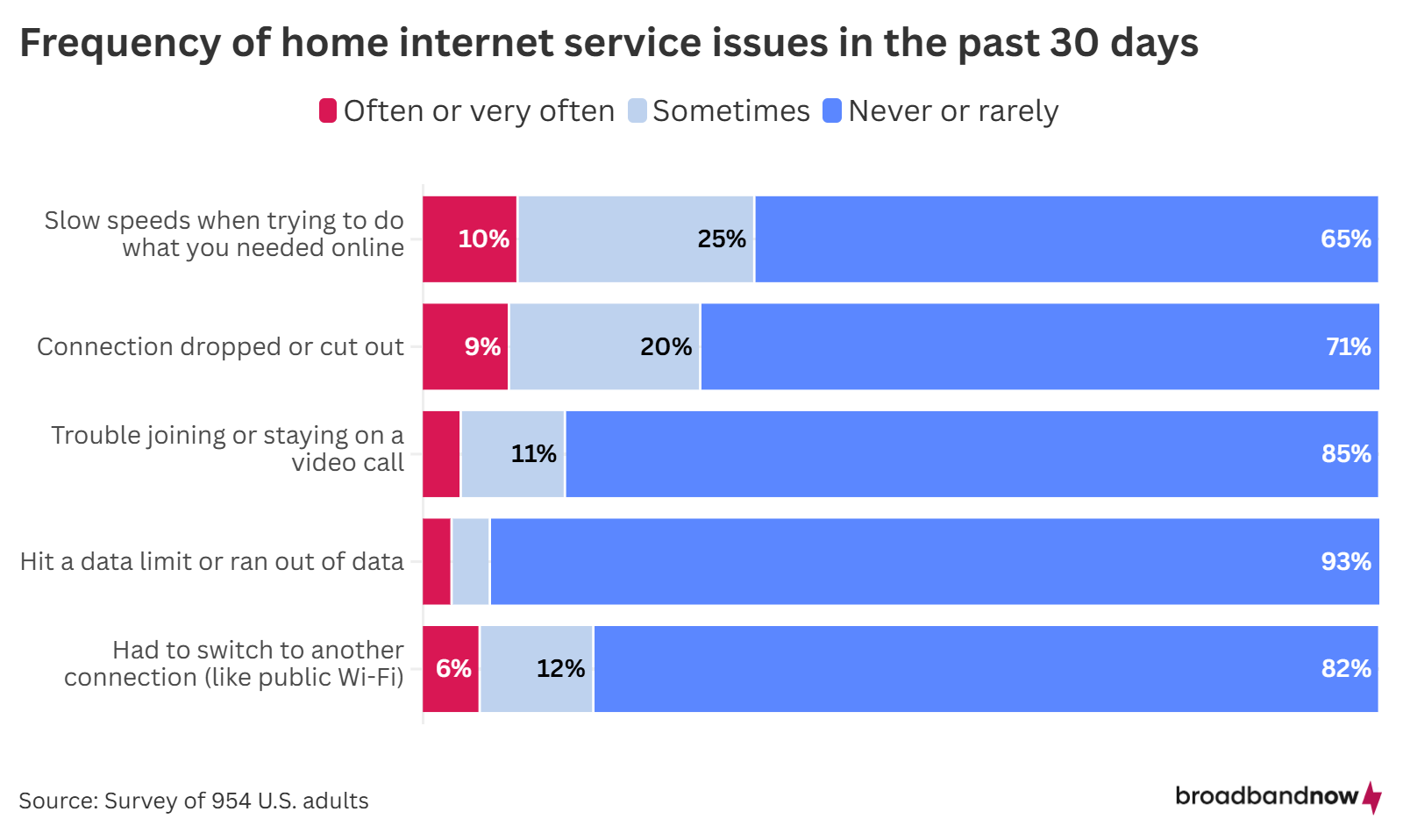

Paying More Doesn’t Always Mean Getting More: Reliability Failures Are Common

Cost isn’t the only frustration. A meaningful portion of Americans regularly experience service disruptions, slow speeds, and video call failures, suggesting that even when people pay $80 or more per month, they aren’t always getting reliable service.

Roughly one in 10 Americans often experience slow speeds (10 percent) or dropped connections (nine percent) in a given month. Given that nearly half of Americans used the internet for healthcare tasks and more than half for work in the past 30 days, these disruptions carry tangible real-world consequences: missed appointments, lost productivity, and failed job applications.

The 16 percent who sometimes or frequently had to switch to a hotspot or public Wi-Fi to finish a task pay a hidden “reliability tax.” These households are effectively paying for backup connectivity on top of their primary plan. Speed and reliability problems are particularly acute in low-competition markets, where providers face little pressure to invest in infrastructure or improve customer service. The FCC’s updated broadband speed benchmark of 100/20 Mbps for fixed services is intended to address adequacy gaps, but millions of Americans remain below that threshold.

What Happened to ACP Recipients After the Program Ended?

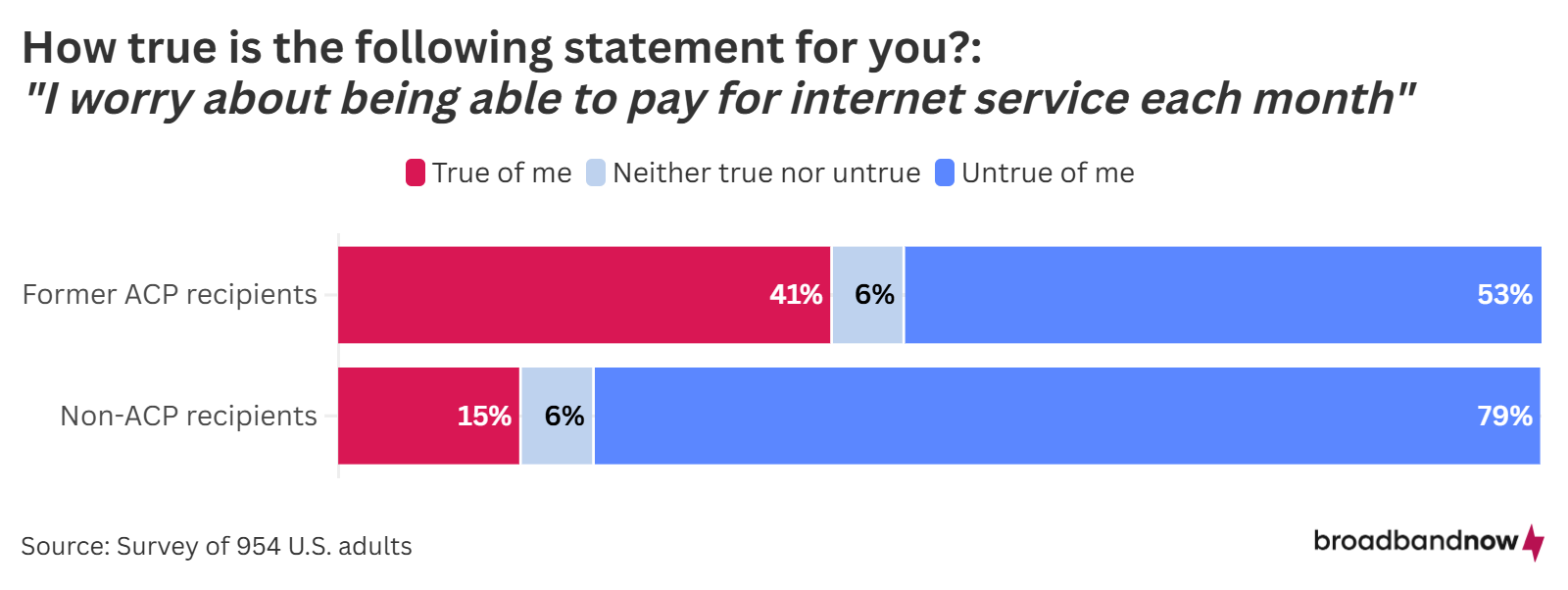

In June 2024, the Affordable Connectivity Program (ACP) officially ended, cutting off a monthly internet subsidy of up to $30/month for most households and $75/month on tribal lands, for approximately 23 million enrolled households. Two years later, the survey data make clear that many former recipients have not recovered and have relied heavily on the program. In fact, 16 percent of respondents in our study had been beneficiaries of the ACP.

41 percent of former ACP recipients worry about paying their internet bill each month, nearly three times the rate of non-recipients (15 percent). More than one in five former recipients (22 percent) say that worry is “very true” of them. Among non-recipients, only three percent say the same.

Former ACP households are also significantly more likely to say their internet plans are inadequate, for themselves and for their children. Without the subsidy, some have likely downgraded to slower, cheaper plans; others may be staying on plans they can no longer comfortably afford.

While several ISPs launched low-income services or programs in the ACP’s wake, including Comcast’s Internet Essentials and other digital equity offerings, the survey data suggests these alternatives have not closed the gap for many households. The ACP ended because Congress did not appropriate additional funding to continue it, and no federal replacement is currently on the horizon.

Methodology

Survey data: BroadbandNow surveyed 954 U.S. adults in March 2026 via an online survey. Respondents reflect a general adult U.S. population. Reported demographics include: Gender (Female n=478, Male n=476); Age groups (18–29 n=184; 30–44 n=250; 45–59 n=284; 60+ n=236); and income brackets (<$50K; $50K–$74,999; $75K–$99,999; >$100K). Reported differences between subgroups were tested for statistical significance and are labeled where applicable.

Limitations: As the survey was conducted online, people without home internet plans are likely underrepresented.

Broadband pricing data: BroadbandNow analyzed active internet-only, residential plans from 2,100+ ISPs. Data reflects plan availability and pricing as of March 25, 2026. Average price per state was calculated across all available plans offered by providers serving that state.

Questions about this study? Contact press@broadbandnow.com to interview an expert.